J. East China Norm. Univ. Philos. Soc. Sci ›› 2007, Vol. 39 ›› Issue (2): 78-81.doi: 10.16382/j.cnki.1000-5579.2007.02.013

Previous Articles Next Articles

Nan XU, De-lei YE

Received:

Online:

Published:

Abstract:

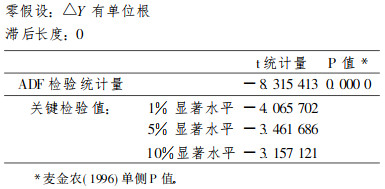

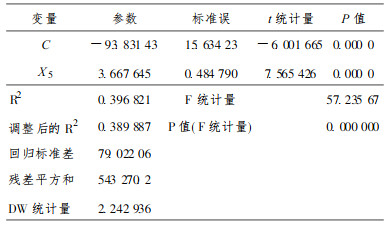

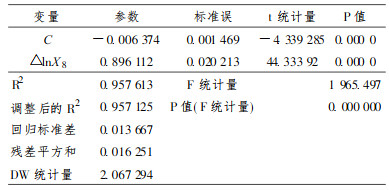

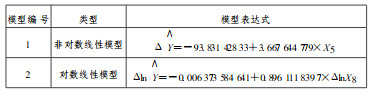

Eight variables such as exchange rate, interest rate, GDP growth rate, trading volume, turnover ratio, P/E ratio, trading volume of funds and tradable market value theoretically related to the index are chosen here as possible explanatory variables, and the modeling strategy is guided by the average economic regression principle in which a model involving only one explanatory variable is first established and more explanatory variables will later be added into the model as long as they do not deteriorate the statistic quality of the model. Linear models and logarithmic linear models that can pass various econometric tests such as ADF, ARCH, and RAMSEY and have no problem of multi - collinearity and self - correlation, are built and compared with respect to goodness of fit. By doing so, it is proved that Shanghai Composite Index is poorly correlevant to macro- economic variables such as exchange rate, interest rate and GDP growth rate, but highly correlevant to micro- market variables such as trading volume, turnover ratio and the like. This conclusion cannot deny the connection between macro economy and stock market. On the contrary, it reflects some structural limitations of Shanghai stock market before its recent reforms.

Key words: econometric model, securities market, Shanghai Composite Index

CLC Number:

F830.91

Nan XU, De-lei YE. An Analysis of Shanghai Securities Composite Index Based on an Econometric Model[J]. J. East China Norm. Univ. Philos. Soc. Sci, 2007, 39(2): 78-81.

/ / Recommend

Add to citation manager EndNote|Reference Manager|ProCite|BibTeX|RefWorks

URL: https://xbzs.ecnu.edu.cn/EN/10.16382/j.cnki.1000-5579.2007.02.013

https://xbzs.ecnu.edu.cn/EN/Y2007/V39/I2/78

"

国家社会科学基金学术期刊资助入选期刊

国家社会科学基金学术期刊资助入选期刊