J. East China Norm. Univ. Philos. Soc. Sci ›› 2007, Vol. 39 ›› Issue (6): 114-116.

Previous Articles Next Articles

Mu-yang HUANG

Received:

Online:

Published:

Abstract:

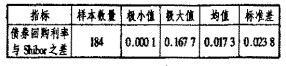

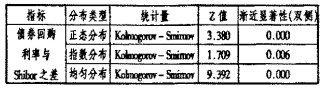

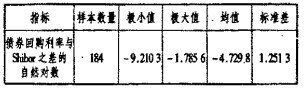

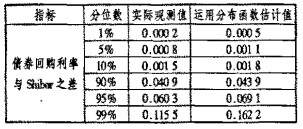

The Inter-Bank Bond Repo Rate and Shibor are two guidance short-term interest rates in China's Monetary Market. They reflect the short-term financing costs of the Inter-bank bond market and the Inter-bank borrowing market respectively. This empirical analysis on the difference between the Inter-Bank Bond Repo Rate and Shibor finds out three indices, i.e., the well-balanced, attention and close attention numerical intervals, which will help the Central Bank monitor risks of the Inter-bank local currency market easier.

Key words: Inter-Bank Bond Repo Rate, Shibor, non-parametric test, method of percentiles, confidence interval estimation

CLC Number:

F830

Mu-yang HUANG. An Empirical Analysis of the Difference between the Inter-Bank Bond Repo Rate and Shibor[J]. J. East China Norm. Univ. Philos. Soc. Sci, 2007, 39(6): 114-116.

/ / Recommend

Add to citation manager EndNote|Reference Manager|ProCite|BibTeX|RefWorks

URL: https://xbzs.ecnu.edu.cn/EN/

https://xbzs.ecnu.edu.cn/EN/Y2007/V39/I6/114

"

国家社会科学基金学术期刊资助入选期刊

国家社会科学基金学术期刊资助入选期刊