J. East China Norm. Univ. Philos. Soc. Sci ›› 2000, Vol. 32 ›› Issue (3): 76-84.doi: 10.16382/j.cnki.1000-5579.2000.03.012

Previous Articles Next Articles

Ping GAO

Received:

Online:

Published:

Abstract:

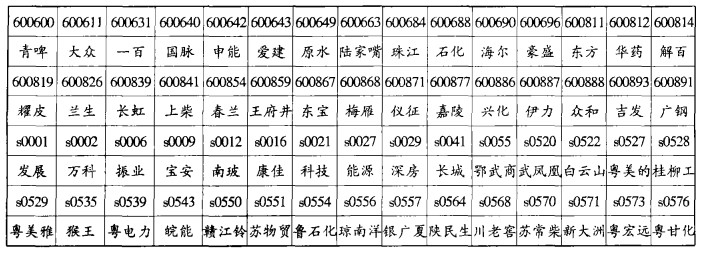

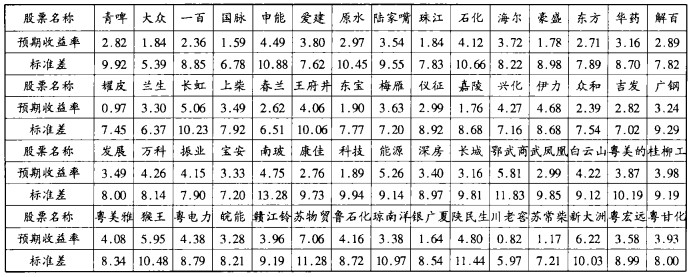

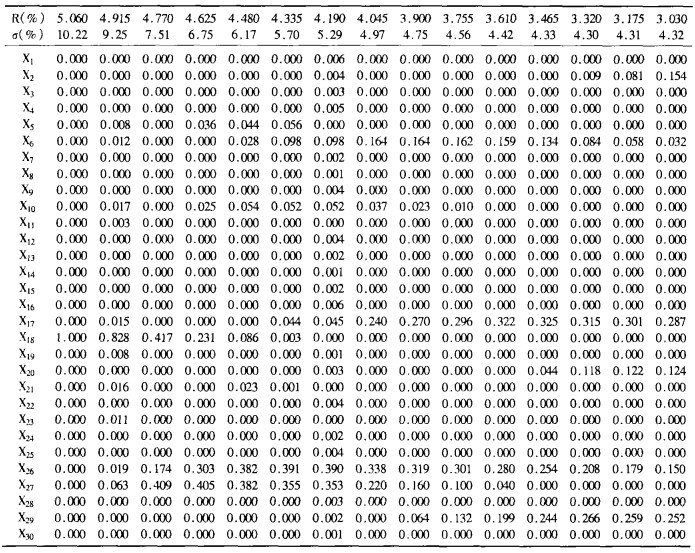

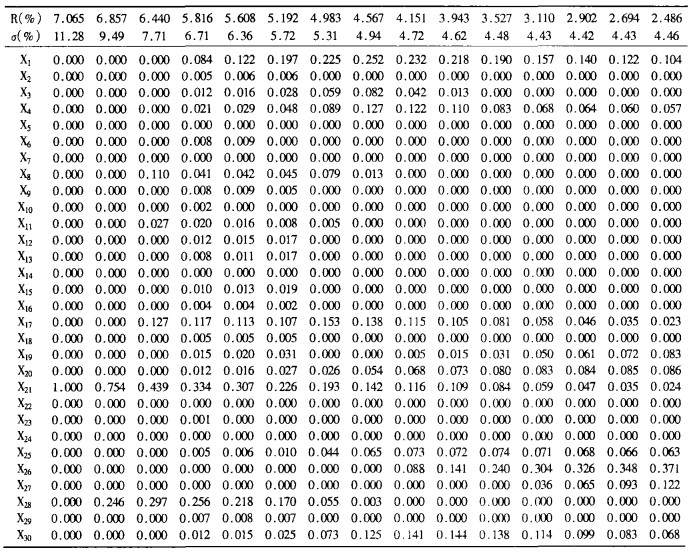

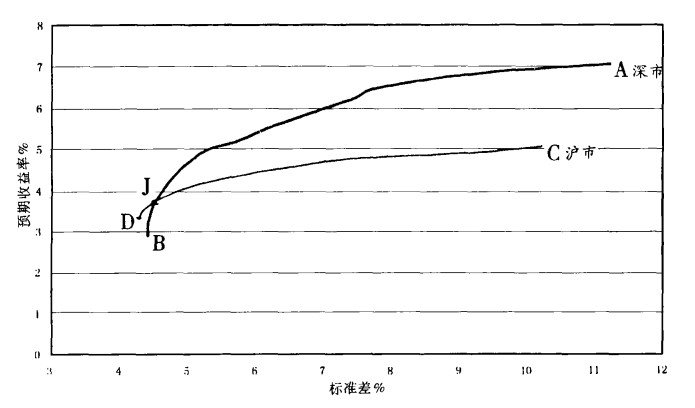

Based on the Mean-Variance Model, this paper analyzes the portfolios of Shanghai and Shenzhen security markets through the 30 model stocks which are sparately selected from two security markets. Quadratic programming algorithm is used in the study of efficient portfolios and efficient frontiers of Shanghai and Shenzhen security markets. After calculating efficient portfolios and drawing efficient frontiers of Shanghai and Shenzhen security markets, we can find a new efficient frontier made up of efficient frontiers of Shanghai and Shenzhen security markets. So we can get some helpful conclusions depending on the new efficient frontier.

Key words: Shanghai and Shenzhen security markets, portfolio, efficient frontier, the Mean-Variance Model

Ping GAO. Portfolio Positive Study of Shanghai and Shenzhen Security Markets[J]. J. East China Norm. Univ. Philos. Soc. Sci, 2000, 32(3): 76-84.

0 / / Recommend

Add to citation manager EndNote|Reference Manager|ProCite|BibTeX|RefWorks

URL: https://xbzs.ecnu.edu.cn/EN/10.16382/j.cnki.1000-5579.2000.03.012

https://xbzs.ecnu.edu.cn/EN/Y2000/V32/I3/76

"

国家社会科学基金学术期刊资助入选期刊

国家社会科学基金学术期刊资助入选期刊